Setting Up Pocket Money Rules by Age

Clear frameworks for deciding how much pocket money kids should get, how often to give it, and what conditions to attach to it at different ages.

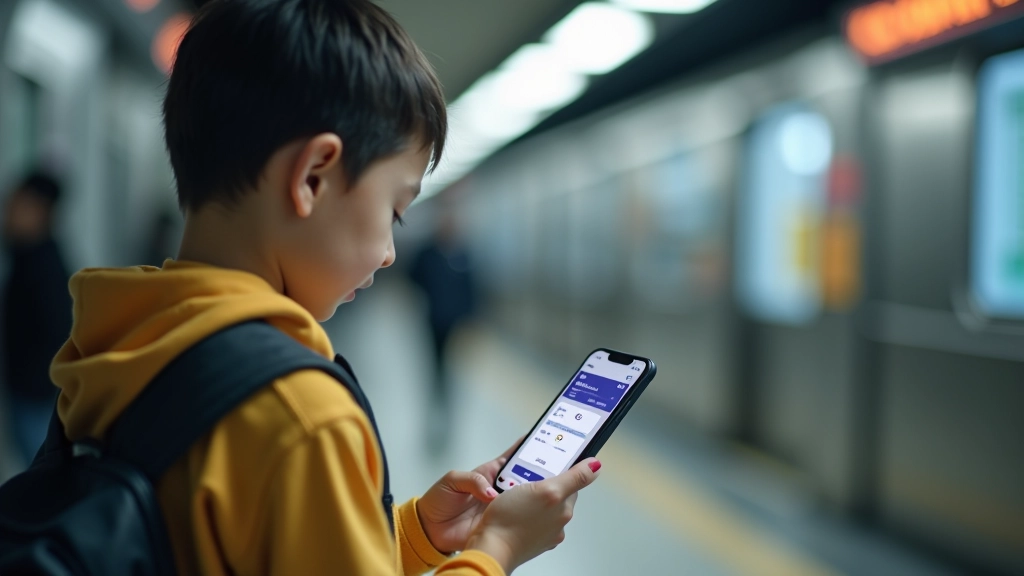

Using Hong Kong’s iconic transit card as a real-world lesson in spending awareness, balance management, and understanding where money actually goes.

Most kids don’t really think about money when they’re swiping a card. It’s just swipe, beep, go. But that’s exactly why the Octopus card is such a powerful teaching opportunity. Unlike cash that disappears visibly from a wallet, the Octopus balance is invisible — which means kids often have no idea how quickly their money vanishes. When you bring awareness to that balance, you’re teaching something fundamental: spending has real consequences.

The Octopus card isn’t just for MTR rides. Your child’s probably using it for school lunch, vending machines, convenience stores, and yes, getting home from school. That’s multiple small transactions throughout the day. Each one is tiny enough to feel inconsequential. But together? That’s where the learning happens. This is real money going somewhere real, and they can actually track it.

The Core Lesson: When money is abstract (a number on a screen), kids spend without thinking. When they actively track it, behavior changes.

Start simple. You don’t need fancy apps or spreadsheets. The goal is just to make the invisible visible.

Get your child their own Octopus card (or add them to yours if they’re younger). This matters. It’s not the same as borrowing your card. When it’s theirs, there’s ownership. They understand that depleting that balance means they’re using their own money.

Next, create a simple tracking method. A notebook works fine. Every few days, they check the balance at a card reader — there’s one at almost every MTR station and convenience store. They write down the date and the remaining balance. That’s it. Over a week or two, the pattern becomes obvious. They’ll see exactly how much is leaving and where.

Some families use a shared spreadsheet. Others just take a photo of the balance display weekly. The method doesn’t matter. What matters is the regular check-in. When a child sees their balance drop from HK$200 to HK$120 in just 5 days, they start asking questions. “Where did it go?” Perfect. That’s the conversation you want.

After two or three weeks of tracking, the real data emerges. You’ll start seeing where the money’s actually going. And it’s rarely what kids expect.

A typical pattern: MTR fare is around HK$10-15 per trip. School lunch might be HK$25-35. But then there’s the convenience store visit. A drink here, a snack there. HK$15 on Tuesday. HK$20 on Wednesday. HK$12 on Thursday. None of these feel significant in the moment. But over a month, that’s easily HK$150-200 just on convenience store impulse purchases.

This is where the teaching magic happens. Sit down with your child and look at the numbers together. Don’t lecture. Just ask questions. “You spent HK$85 on snacks this week. Did you know that?” Most won’t. “What could you do differently?” Let them figure it out. They’re not dumb — they just didn’t have the data before.

Some kids will decide to bring snacks from home. Others will set a weekly convenience store budget. A few will realize they don’t actually want most of that stuff — they were just bored or their friends were buying. That realization is worth more than any lecture.

Once the tracking habit is established, layer in goals. This transforms the Octopus card from just a transit payment method into an actual savings and spending management tool.

Ask your child: “If you spent less on convenience store snacks, what could you save for?” Maybe they want to buy something specific. A new gaming item. Concert tickets. Doesn’t matter. Give them a target. “If you keep your card balance above HK$100 for two weeks, we’ll know you’re managing it well. What does that mean you need to change?”

This isn’t about restriction or punishment. It’s about choice with consequences. They understand that spending HK$20 on impulse snacks means they can’t buy something they actually want. That’s real-world financial literacy right there.

Some families set up a simple reward system. Keep your balance in a target range for a month, and maybe they get a bonus top-up or a small privilege. Others just use the tracking itself as feedback. Either way, the Octopus card becomes a tool for managing resources, not just a convenience.

The beauty of using the Octopus card is that you can adapt it for different ages. A primary school child might just check their balance weekly and draw a simple graph. A secondary student can do deeper analysis — breaking spending into categories and setting realistic budgets.

For younger kids (ages 7-9), keep it visual. A simple chart showing the balance going down is often enough. They start understanding that money is finite. By ages 10-12, they can handle basic tracking and can see the connection between their choices and their balance. Teenagers? They’re ready for real budgeting. Help them categorize their spending — transport, food, leisure, other — and see where their money actually goes.

Don’t expect perfection. Kids will forget to check sometimes. They’ll spend without thinking occasionally. That’s normal. The point isn’t to control them — it’s to give them information and let them make better decisions. Some months they’ll do great. Other months they’ll blow through their balance and learn the hard way. Both are valuable lessons.

The conversations matter more than the tracking itself. “Why do you think you spent more this week?” “What would make this easier?” “Do you feel good about where your money went?” These questions build awareness. And awareness is the foundation of better financial decisions.

The Octopus card tracking system isn’t complicated. It’s not expensive. It doesn’t require apps or special tools. What it does is create visibility. And visibility changes behavior.

The real power comes from making it routine. Check the balance every few days. Talk about the numbers. Celebrate when they hit a goal. Learn when they don’t. Over time, kids internalize the lesson. They start thinking about spending before they swipe the card, not after. They understand that money is real, that it runs out, and that their choices matter.

By the time they’re teenagers, this habit becomes automatic. They’re already thinking about money management without you having to push. And that’s exactly what financial literacy looks like — not rules or lectures, but actual awareness and intentional decision-making. The Octopus card is just the tool. The real lesson is teaching kids to think about their money. Once they do that, everything else follows.

This article provides general educational information about teaching children money awareness through tracking and budgeting tools. It’s not financial advice, and it shouldn’t replace professional guidance when needed. Every child develops at their own pace, and what works for one family may need adjustment for another. If you have specific concerns about your child’s financial behavior or understanding, consider consulting with an educational specialist or financial counselor who can provide personalized guidance.